Introduction

Recession discussions, interest rate hikes, economic consequences of the war: Key events of the third quarter?

- In the last quarter, monetary tightening and recession discussions, which have been the main agenda throughout the year, remained on the agenda. In particular, the policies of the US Federal Reserve were the most important factor affecting the markets in this quarter. With the hope that the Fed will step back from its tight monetary policy, markets have recovered from the lows of mid-June. However, hawkish messages from the Fed officials since mid-August and the signals given at the Fed meeting that the stance would continue, caused a new selling wave in the markets.

- Looking at the current outlook, economists, strategists and fund managers see a 50-60% chance of the US economy entering recession in the next 12 months, according to various market surveys (over 70% probability for the European economy). Professor Steve Hanke of Johns Hopkins University predicts a much higher 80% probability of the US economy going into recession within 12 months. Hanke states that the reason for this is that M2 money supply growth turned negative with the rapid withdrawal of liquidity following the extreme monetary expansion in 2020.

- In this report, we reviewed the latest status of some macro indicators that stood out as reliable recession indicators in the past and evaluated what might happen in the global economy and markets in the upcoming period. The aforementioned indicators can be summarized as the interest increase rate of the FED, the shape of the yield curve, consumer confidence, the unemployment rate, and especially the level and change of oil prices. On the other hand, we shared the latest developments in the energy, metal and food sectors that stood out in the last quarter and our expectations for the upcoming period.

- In the upcoming period, we think that the mutual sanctions between the USA – EU and Russia due to the Ukraine war may continue, which will keep the upward risks on energy and food commodity prices hold high. Considering the upside risks related to tension between Russia and Ukraine, we expect that the price of Brent oil per barrel will be around $95 by the end of the year. We expect the FED to maintain its inflation-oriented monetary policy stance and to keep the policy rate high until at least the end of 2023. Last but not least, we assume that vaccines will remain effective despite virus mutations from Covid-19.

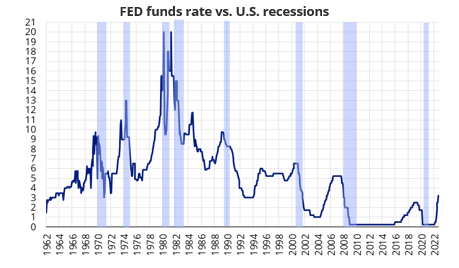

- Latest FOMC meeting on 21 September altered the investment sentiment significantly, as the FED clearly indicated that it intends to keep the policy rate at higher and longer than previously expected (desired) by markets. Remembering that the FED's forecast for December 2021 was 0.9%, the tightening in the monetary policy stance of the FED since the beginning of the year is more clearly understood.

- FED’s aggressive tightening cycle, along with the ongoing implications of the Russia/Ukraine war (potential pressure on commodity prices, natural gas in particular) and China’s souring economic outlook have significantly increased the recession expectations, in the U.S. and worldwide.

- In particular, a potential resurgence of oil prices (e.g. towards USD100bbl levels) due to external and geopolitical factors has the potential to drag the U.S. and World economy into a recessionary or actually a stagflationary era, similar to the one in the 1970s (though to a lesser extent). This would surely have significant implications for the general risk sentiment and economic conditions, borrowing costs of the indebted (EM) economies, in particular.

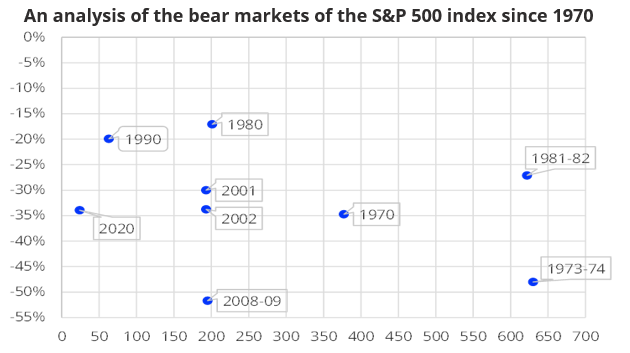

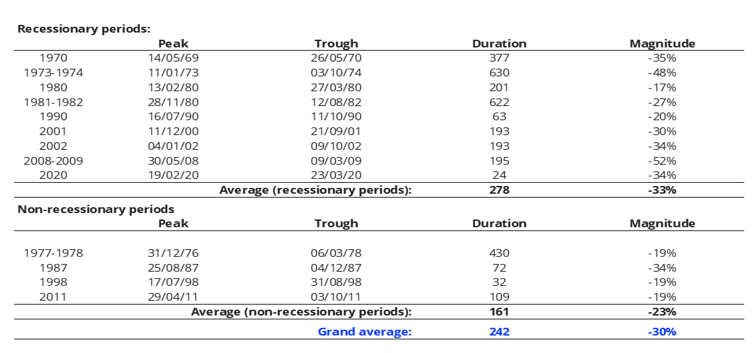

- Examining the bear markets of the S&P 500 that took place since 1970, we see that the average loss throughout recessionary periods approached roughly 33%. Accordingly, historical data suggests that there may be a lot of room (about 15-20%) for further declines in the US stock markets in the days ahead (barring short-term corrections). The downtrend may actually strengthen in case of an energy price-driven recession. Yet, past experience also shows that the recovery may be very fast from the bottom levels. Accordingly, we may also witness a rapid rise in the S&P-500 index, if central banks soften their stances as the signs of recession become more evident. In this respect, the course of energy prices will be critical, in our view.

Economic Outlook: Global

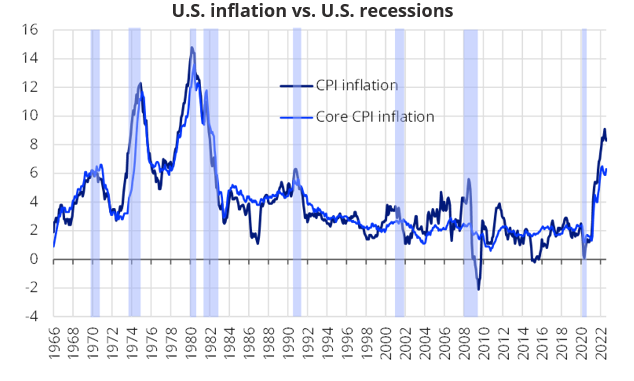

Despite partial pullbacks in energy and commodity prices, global inflation continues to hover above expectations and close to peak levels.

- Although the CPI inflation retreated to 8.3% in August after peaking at 9.1% in June, surpassed market expectations, and core CPI inflation increased to 6.3% from 5.9%. As a result, rate hike expectations from the FED shifted higher along with hawkish messages from FED officials.

- Since the 1950s, the US economy has tipped into a recession within two years every time inflation has exceeded 4%. This is due to the fact that high inflation forces the FED to implement an aggressive rate hike cycle (bringing the policy rate above the neutral rate), causing a recession and a sharply higher unemployment rate.

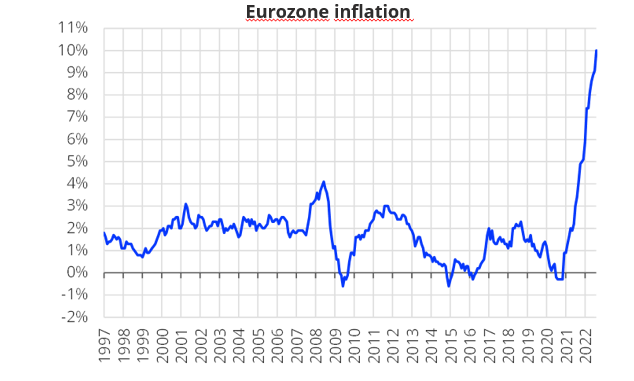

- CPI inflation in the Eurozone in Europe rose to its highest level (4-5 times its historical average) since the transition to the Euro, most particularly due to the dramatic rise in energy costs.

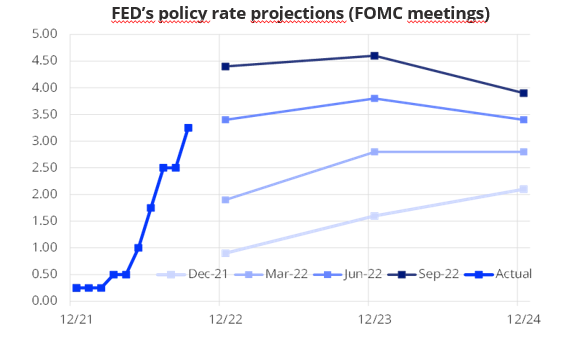

FED consistently upgraded its policy rate projections in recent FOMC meetings

- The FED revised its policy rate projections to 4.4% from 3.4% for the end of 2022 and to 4.6% from 3.8% for 2023 at its last FOMC meeting on September 21. Recall that the FED's such projections for December 2021 were 0.9% and 1.6%, which indicates the significant evolution of the FED’s monetary policy stance.

- FED now predicts the core inflation indicator (core PCE) at 4.5%, which was predicted as 2.7% at the end of 2021, now predicts 4.5%. The forecast for 2023, on the other hand, increased from 2.3% to 3.1% over the same period.

- The FED in its latest FOMC meeting also reduced its 2022 GDP growth forecast to as low as 0.2%. Note that this was as high as 4.0% at the last meeting of 2021. The Fed expects the US economy to grow by 1.2% in 2023.

- The Fed expects the unemployment rate, which is currently at a low of 3.5%, to peak at 4.4% in 2023.

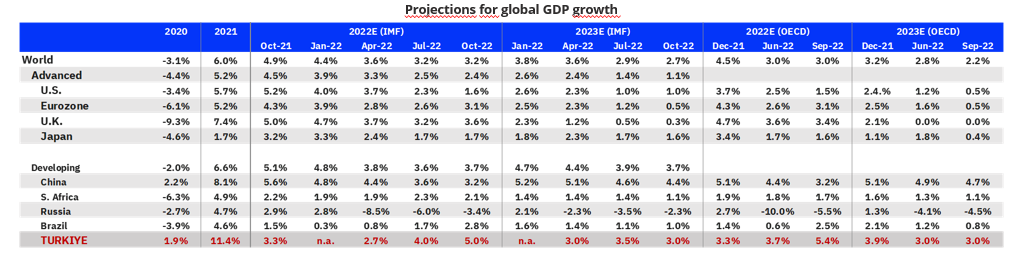

Global GDP growth projections are being revised down as central banks further tighten monetary policy

- In its Economic Outlook report published in September, the OECD kept its global growth forecast for 2022 constant at 3.0%, while lowering its 2023 forecast to 2.2% from 2.8% in June and down from 3.2% back in December 2021. Although the OECD kept its 2022 Global growth forecast constant, it significantly lowered its forecasts for the US economy and the Chinese economy. The OECD now projects the U.S. growth for 2022 as 1.5%, down from 2.5% and 3.7% in the prior reports, while China's growth forecast was revised from 5.1% to 4.4% and then to 3.2%. OECD’s 2023 growth forecasts for the U.S. and Eurozone stand at 0.5% each.

- The IMF, on the other hand, kept its Global growth forecast constant at 3.2% for 2022 in its October World Economic Outlook report, while lowering it to 2.7% from 2.9% for 2023. The IMF's 2023 US growth forecast is 1.0%, while the Eurozone growth forecast is 0.5%.

History suggests a so-called “soft landing” is a rare outcome after FED’s monetary tightening cycles

- History suggests a so-called “soft landing” is a rare outcome after FED’s monetary tightening cycles. According to New York Federal Reserve, 11 out of 15 previous tightening cycles (since 1955) have ended up with recessions. Looking at the period after 1970, FED initiated a monetary tightening cycle 10 times, 7 of which have resulted in recession (although all recessions may not be necessarily related to purely FED’s tightening). Although, FED’s monetary tightening cycles have often led to a recession, please note that the period between the start of the tightening and start of the recession varies significantly, ranging from 10 months to 50 months.

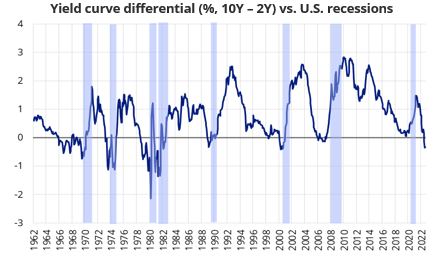

- All recessions since the 1960s have been preceded by an inverted yield curve. Yet, its reliability significantly weakens for predicting the timing of the potential recession, as yield curve may actually remain inverted for too long before the economy heads into recession. For instance, we see that ahead of the 1970 recession, the yield curve has actually remained inverted for some 1,456 days (about 4 years) before the economy dipped into recession. Looking at more recent history, the yield curve had been inverted by 670 days (almost 2 years) ahead of the 2008-09 Global Financial Crisis. In the previous 9 recessions, the average timespan between yield curve inversions and recessions has been 592 days (about 1.5 years), although the duration varied between 239 days and 1,456 days. Note that the current yield curve inversion has been ongoing for the past 3 months (since 06 Jul).

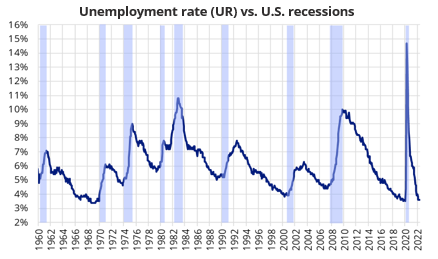

All recessions have actually occurred right after the unemployment rate (UR) dipped

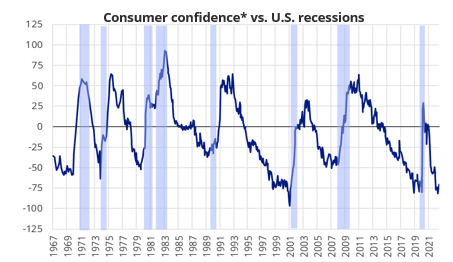

- The difference between the two components of the consumer confidence index (released by the Conference Board), namely the «expectations index» and the «present situation index» has been hovering around historically low levels for some time, which has also been a reliable recession precursor in recent history.

- Unemployment rate (UR) has actually been a «lagging» not a «leading» indicator of a recession. Yet, it may still be a reliable precursor for recession, as UR has always been close to its trough level right before the start of the recession. Since the 1950s, the US economy has tipped into a recession within two years every time UR has fallen below 5%.

- The «Sahm Rule» signals the start of a recession when the 3-month moving average of the national unemployment rate (U3) rises by 0.50 percentage points or more relative to its low during the previous 12 months. Accordingly, it can be argued that currently, the historically low levels of UR may not be a relieving factor against recession. On the contrary, it could be a harbinger of an impending recession.

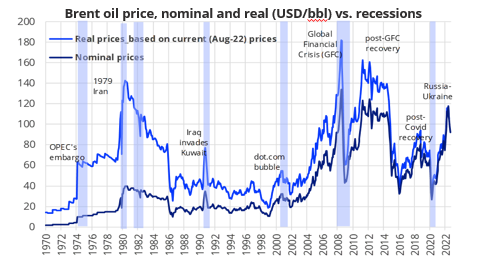

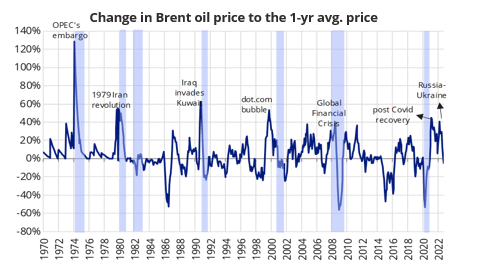

Oil price spikes have preceded seven of the past nine US recessions

- Looking at oil prices in real terms, i.e., adjusted for the US CPI inflation, although the current levels of oil prices are significantly high, they still remain well below the levels witnessed during the 1979 Oil Crisis, 2009 Global Financial Crisis (GFC) and post-GFC recovery period. The resurgence of oil prices (e.g. towards USD100bbl levels) due to external and geopolitical factors has the potential to drag the U.S. and World economy into recessionary or a stagflationary era, similar to the one in the 1970s (though to a lesser extent). This would surely have significant implications for the general risk sentiment and economic conditions, borrowing costs of the indebted (EM) economies, in particular.

- Apart from the price level, oil price shocks (the level change from the previous one or two years) also do matter, as oil price spikes have preceded seven of the past nine US recessions. In that stance, the doubling of global crude oil prices over the past year may be a cause for concern for the probability of a recession. Despite the recent pullback in oil prices from peak levels, its sustainability remains unclear, as we think that the potential for oil prices to rise again due to the ongoing Russia-Ukraine war is maintained.

Overview of Commodities

Historical data suggests that there may be a lot of room (about 15-20%) for further declines in the US stock markets

- The S&P 500 index recently tested new trough levels although it had recovered by about 17% from mid-June to mid-August. The index is currently about 25% below the peak level achieved just at the beginning of the year. This suggests that the S&P index is still hovering at a bear market.

- Examining the bear markets of the S&P 500 that took place since 1970, we see that downtrends lasted for an average of about 8 months, and the average loss throughout these periods approached roughly 30%. Yet, the magnitude and the duration of downtrends are more severe amidst recessionary periods with an average duration of 278 days and an average loss of 33%, while these are 161 days and -23% for non-recessionary periods. Accordingly, historical data suggests that there may be a lot of room (about 15-20%) for further declines in the US stock markets in the days ahead, barring short-term corrections (although we think that each period should be evaluated on its own terms). The downtrend may actually strengthen in case of an energy price-driven recession. For instance, during the 1973-74 oil price shock, the total sell-off in the S&P-500 index reached about 48% in a time span of about 630 days

- All these being said, past experience also shows that the recovery may be very fast from the bottom levels. Accordingly, we may also witness a rapid rise in the S&P-500, if central banks soften their stances as the signs of recession become more evident. In this respect, the course of energy prices will be critical, in our view.

Fossil Energy Sector

The biggest current risk in fossil energy pricing is the course of the Russia-Ukraine war. Russia, one of the world's largest fossil energy exporter, announced in September that it had cut off the gas flow to Europe for a while, citing maintenance on its gas lines. We think that if the risks of geopolitical war continue and worsen, Russia may stop gas exports again. We believe that the rise in gas prices cannot be prevented if this situation occurs.

According to estimates, the 2 million barrels per day production cut that OPEC+ agreed to at its most recent meeting will decrease the world's supply of oil and shrink the market.

It has been revealed that 10 million barrels of oil will be supplied to the market in November on Biden's orders, despite the USA's opposition to OPEC's plan to reduce supplies. Diplomatic and political decisions can be shown as the most important risks that may affect the course of oil prices in the upcoming period. Given that Russia exports not only gas but also oil, we believe that we may observe an increase in volatility in oil prices.

We estimate a sharp decline in the imports of fossil energy from Russia to Europe over the next few years, assuming that geopolitical risks remain current. Retesting the highest level of oil is a significant risk element if oil exporters, particularly Arab nations, continue to reduce production and encounter supply shocks. In conclusion, even though fears about the recession are driving down the price of fossil fuels, geopolitical dangers remain in place.

We can infer that a significant portion of the highest inflation rates ever recorded in the USA, Europe, and England can be linked to changes in oil prices. The disclosure of the highest inflation levels ever in the USA, UK, and Europe was influenced by the increases in the cost of fossil fuels. High inflation rates have an impact on central banks' tightening policies since they are influenced by energy prices. In this circumstance, the sharp rate hikes are feeding recession fears.

Industrial Metals Sector

Starting 2022 with a positive outlook, industrial metal prices are losing strength due to the decreasing demand as a result of the global tightening policies of the central banks. Due to the concerns about the global economy and the decline in the growth forecasts for 2023 announced by the IMF, we anticipate that prices may not recover for a while due to the shrinking demand for iron and steel.

High inflation, rising interest rates, supply chain disruptions and the Russia-Ukraine war have weakened the growth outlook for industrial companies this year. While the decline in consumer spending does have an impact on manufacturers, the oil crisis in Europe and the stagnation in Chinese economy pose a threat to foreign demand. Nevertheless, the relatively strong stance in employment rates and industrial production data in US, serves as a counterbalance.

We believe that the industrial metals sector may recover if we see a decline in global energy prices in upcoming periods and the likelihood of recession decreases due to the course of interest rate hikes.

While the S&P 500 has fallen by 11.5% since the second half of the year, industrial metals stocks maintain their downward momentum in line with the volatile course in the indices. Steel Dynamics and Nucor Corp. had outperformed other stocks with %6.5 and %9,7 decline respectively. US Steel Corp. was down 23% and ArcelorMittal SA lost more than the index with losses of 31.8%.

Renewable Energy Sector

Global renewable capacity additions are expected to remain flat compared to 2022 unless new and stronger policies are implemented in 2023. Solar power is projected to reach around 200 GW in 2023 and set another record as wind and bioenergy expansion hold steady. However, geopolitical and macroeconomic challenges add to the uncertainties over the forecasts for the use of renewable energy in 2023.

The rise in oil, natural gas, and coal prices causes the production costs of materials produced for renewable technologies to increase. On the other hand, it can be said that renewable energy costs do not hinder their competitiveness as fossil fuel and electricity prices have increased much faster since the last quarter of 2021.

The process of Russia's invasion of Ukraine forced the European Union and the whole world to work on clean energy in order to reduce its energy dependence on Russia. More widespread use of renewable energy has become a strategic imperative for many countries, especially in the European Union. Many European Union countries have announced a transition plan to renewable energy to reduce the European Union's dependence on the energy sector by 2023.

Renewable energy capacity is expected to increase by more than 8% compared to last year by the end of 2022 and to cross the 300 GW limit for the first time. On the other hand, the solar energy sector is expected to account for 60% of the increase in global renewable capacity this year, with a 25% gain over last year. Projects account for almost two-thirds of the overall renewable energy expansion in 2022 and are driven mostly by a strong policy environment enabling faster deployment in China and the European Union.

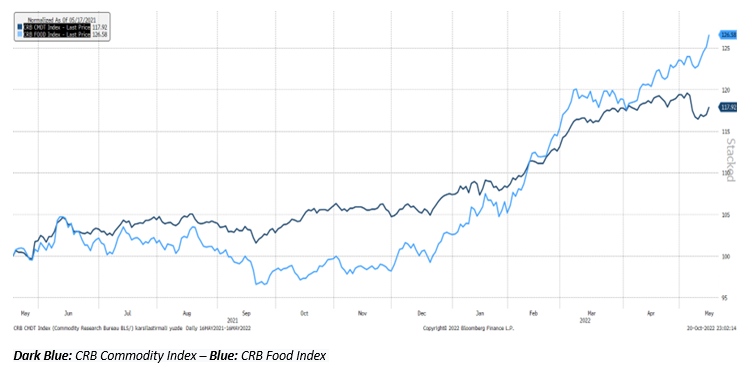

Agriculture Sector

According to the FAO report, agricultural production is expected to increase by 1.1% annually over the next ten years. But a prolonged rise in energy and agricultural commodity prices could increase production costs, limiting productivity in the coming years. On the other hand, global food consumption is expected to increase by 1.4% annually over the next ten years. This increase is expected to be due to population growth. While most of the demand continues to come from low- and middle-income countries, slowing population growth in high-income countries may limit demand from this side.

After the pandemic, the recovery in demand and the decrease in supply due to the Russia-Ukraine war caused agricultural commodity prices to rise. Analyst forecasts indicate that production in Ukraine will decrease in the period 2022-2023, and export rates in both Ukraine and Russia will decrease.

The Russia-Ukraine war affected the feed, fertilizer, and energy markets as well as the food industry. The war has altered commodity prices to keep prices high until the end of 2024, exacerbating food insecurity and inflation.

Some countries have begun to develop policies to ease the resulting pressures on producers and consumers. For example, some measures, such as reducing import-export restrictions, facilitated the food supply.

In the current situation, fertilizer prices have started to rise again after a short relief in the summer of 2022. In addition to rising energy prices, policy measures such as export restrictions may limit the global availability of fertilizers. In the coming months, access to fertilizers may become more difficult, which could affect food production for many crops in different regions. Because Russia is the country that exports 38% of potash fertilizers, 17% of compound fertilizers, and 15% of nitrogen fertilizers.

Ready to start your trading journey? Create your account in minutes and start trading on MetaTrader 4 or 5.

Trade Now